Credit risk analysis is evolving. Although the basic tenet of assessing whether an issuer can pay back its obligations on time and in full still holds, the global fixed income (FI) community is increasingly seeking ways to factor in sustainability considerations when allocating capital and managing risks.

As a first step, this requires ensuring that environmental, social and governance (ESG) factors, where material, are appropriately reflected in credit risk analysis.

The PRI has been working with investors and credit rating agencies (CRAs) since the launch of the ESG in Credit Ratings Initiative in 2016 to promote understanding of practices, identify gaps in the consideration of ESG factors in credit risk analysis, and find ways to address those gaps.

This investor-CRA dialogue has highlighted that ESG consideration in credit risk analysis is still not addressed consistently and systematically by all FI market participants. However, it has also brought to light that:

- many positive developments are gaining rapid momentum – including expanding resources and increasing transparency efforts by many investors and CRAs to explain how ESG factors feature in their analysis;

- the idea that ESG consideration is part of a holistic approach to assessing credit risk is gaining traction;

- perceptions are shifting and ESG signals are beginning to be used not only to manage downside risks but also to spot investment opportunities; and

- FI investment and credit ratings have different objectives: whereas a credit rating will only include ESG factors if material to credit risk, investors looking for guidance on ESG factors in a FI investment may also use standalone ESG scores and assessments.

This report, the third in a three-part series, focuses on the emerging solutions discussed during 15 investor-CRA forums that the PRI organised globally, targeting credit practitioners, to address four apparent investor-CRA disconnects, i.e. areas where investors and CRAs seemed to have different views at the start of the initiative (see below). The report builds on part one, which described the state of play of ESG consideration in credit risk analysis, and part two, which focused on the results of roundtable discussions exploring those disconnects.

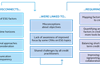

Some of the disconnects have emerged as misconceptions or signs of calls for greater transparency and increased communication between investors and CRAs. It also transpired that some are shared challenges that credit practitioners face as they build a more systematic framework to consider ESG factors, and that more work needs to be done to:

- assess ESG factor materiality and, in the case of investors, performance attribution;

- monitor the ESG triggers that may alter credit risk assessments and threaten the sustainability of business models over the long term; and

- reach a minimum level of ESG standardisation.

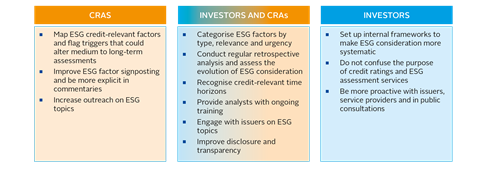

Against this backdrop, the PRI has compiled a list of action areas, which are aimed at improving the process and output of ESG consideration in credit risk analysis. Some areas target both CRAs and investors, and others are more tailored to either stakeholder. The figure below contains some highlights.

See the section Applying theory to practice to read the full recommendations.

The list should be treated as best-in-class practice and does not suggest a one-size-fits-all approach to the consideration of ESG factors in credit risk analysis, as the implications of ESG factors (current or potential) on issuer creditworthiness depend on the specific characteristics of each entity. Moreover, while there are areas of common ground between investors and CRAs, there are also differences (such as in terms of the purpose, duties and legal boundaries of their analysis). For instance, credit ratings exclusively reflect an assessment of an issuer’s creditworthiness and CRAs must be allowed to maintain full independence in determining which criteria may be material to their ratings, as per the ESG in Credit Ratings Statement. Finally, among institutional investors, sensitivities to ESG factors vary depending on whether the investment objectives are those of asset owners (AOs) or asset managers (AMs).

While some actions can be implemented quicker than others, the PRI encourages organisations to prioritise them depending on their starting point, size and resources – but, importantly, to continue to demonstrate change. Indeed, some market players – notably the large, global CRAs, some specialised ones as well as advanced investors – have already made visible progress on many aspects of the recommendations, as documented by this report and the two previous iterations. In this case, the list represents a guideline to continue or enhance practices. Nevertheless, this better starting point should be no excuse for complacency.

This report also contains new evidence of CRA rating opinions that reference ESG factors explicitly when they have contributed to a change in rating or rating outlook, adding to the list of examples that the PRI published in part two (see section on CRA examples). It includes 15 additional case studies highlighting how investors that have already implemented a framework to systematically assess ESG factors in credit risk analysis have used it to address one or more of the aforementioned action areas before reaching an investment conclusion (see section on investor case studies). Some of the case studies are on sovereign credit risk, which a panel session at the 2017 PRI in Person conference in Berlin, as well as the London and Paris roundtables, started to address (see section on sovereign versus corporate credit risk).

Finally, the regional roundtables that were held after the publication of part two highlight that ESG awareness, or the call for ESG integration in credit analysis, differs across jurisdictions and regions (see section on regional colour from the PRI forums).

Going forward, the initiative intends to focus on broadening the dialogue between CRAs and FI investors to bond issuers to advance understanding of the materiality of ESG factors to credit risk, and promote engagement, the development of common terminology and enhanced data disclosure. The PRI plans to continue monitoring progress and provide a platform to share it.

We encourage active involvement in the work that lies ahead through feedback, sharing best practices and participating in the debate.

Downloads

ESG, credit risk and ratings - from disconnects to action areas

PDF, Size 3.5 mb转变观念:ESG、信用风险 与评级 第3部分:从脱节迈向行动领域

PDF, Size 3.59 mb変化する展望 第3部:ギャップを埋めるための行動(概要)

PDF, Size 1.41 mb

ESG, credit risk and ratings: part 3 - from disconnects to action areas

- 1

Currently reading

Currently readingExecutive summary

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10

- 11

- 12

- 13

- 14

- 15

- 16

- 17

- 18

- 19

- 20

- 21

- 22

- 23

- 24

- 25