Nature

Nature provides essential services – such as food, clean air and energy – that we all rely on. For investors, the ability to optimise risk-adjusted returns to end-clients and beneficiaries both depends on and impacts nature.

Nature programmes and investor action

Nature in responsible investments

Nature provides ecosystem services that benefit businesses and society. The investment value chain, and investors’ ability to optimise risk-adjusted returns to end-clients and beneficiaries, depends on and impacts nature.

Investing for nature: Resource hub

The PRI has developed a resource hub hosting its own guides, initiatives, blogs and webinars as well as relevant resources from partner organisations, to help PRI signatories find relevant guidance in their efforts to integrate nature into decision-making.

Spring

Spring is a PRI stewardship initiative for nature, convening investors to use their influence to halt and reverse global biodiversity loss by 2030

Nature Reference Group

The Nature Reference Group, with around 70 PRI members, facilitates discussions on investment practices, tools, disclosure framework and initiatives (full Terms of Reference).

Nature Policy Roadmap: Policy recommendations for scaling up investor action for nature

This discussion paper sets out the importance of nature to economic and social systems, its relevance to responsible investors and the PRI’s approach to nature policy.

Nature Positive Initiative

The PRI is part of the Nature Positive Initiative, supporting broader, longer-term efforts to deliver nature-positive outcomes by halting and reversing nature loss.

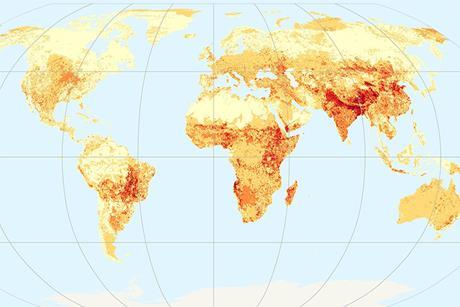

Mapping natural capital depletion

The PRI and UNEP-WCMC have developed maps to showcase hotspots of relative natural capital depletion on a global scale, available for visualisation in ENCORE – an interactive, online tool that highlights how businesses may be exposed to accelerating environmental change.

Investor initiative for sustainable forests: engagement results

The PRI-Ceres partnership aimed to tackle commodity-driven deforestation within cattle and soybean supply chains at investee companies

PRI investor working group on Sustainable Commodities

The PRI has previously coordinated collaborative investor engagements on sustainable commodities, including on palm oil, soy, and cattle supply chains. The investor expectations statements set out their disclosure and practice expectations of companies operating within these supply chains; and have been signed by more than 50 investors representing more than US$ 6 trillion in assets under management. The engagement results from the PRI-Ceres partnership to tackle commodity-driven deforestation within cattle and soybean supply chains at investee companies are available here.

Related resources

An introduction to responsible investment: Biodiversity for asset owners

Introducing biodiversity to asset owners, focusing on drivers of biodiversity loss.

Developing a biodiversity policy: A technical guide for asset owners and investment managers

How institutional investors can integrate biodiversity considerations into their responsible investment policies and investment processes

Blogs

- Previous

- Next

Webinars

- Previous

- Next

Case studies

- Previous

- Next

- The PRI is an investor initiative in partnership with UNEP Finance Initiative and UN Global Compact.

- PRI Association, 1st Floor 20 Wood Street, London EC2V 7AF United Kingdom

- Company no: 7207947

- +44 (0)20 3714 3141

- [email protected]